Unlocking Growth and Security: The Crucial Role of KYC/KYB in Modern Business Transactions

In today’s fast-paced and interconnected business landscape, making payments and conducting transactions with contractors and partners is more seamless than ever before.

In today’s fast-paced and interconnected business landscape, making payments and conducting transactions with contractors and partners is more seamless than ever before. However, this convenience brings with it a host of challenges, especially in the realm of financial security and regulatory compliance. For businesses, ensuring that they “Know Your Customer” (KYC) and “Know Your Business” (KYB) is not just a best practice—it’s a fundamental necessity.

In this era of heightened scrutiny, understanding the importance of KYC and KYB processes has become paramount. It’s not just about ticking regulatory boxes; it’s about safeguarding your business against risks, fraud, and reputational damage. But how can businesses strike the right balance between compliance and efficiency?

A fully compliant fintech solution like Payment Labs can be a game-changer that fully automates and streamlines the KYC and KYB processes, making it easier, more cost-effective, and less prone to errors. In this blog post, we’ll delve into why businesses need to grasp the significance of KYC and KYB when making payments, and how embracing compliant fintechs like Payment Labs can reshape the way you do business. Join us on this journey as we explore the intersection of financial security, efficiency, and growth.

What is KYC (“Know Your Customer”)?

KYC stands for “Know Your Customer” or “Know Your Client.” It is a process that businesses and financial institutions use to verify the identity of their customers or clients, whether they are other businesses or persons, before engaging in financial transactions or providing services. KYC is about knowing the individual(s) involved in the business customer, such as the CEO, Signing Officer, or Beneficial Owner(s). For customers that are individuals, KYC is to confirm that individuals pass the necessary identity verification and compliance checks to conduct business transactions legally. KYC procedures are typically in place to prevent fraud, money laundering, terrorist financing, and other illegal activities.

KYC involves collecting and verifying various pieces of information about an individual including:

1. Identity Verification: This may include collecting government-issued identification documents such as passports, driver’s licenses, or national ID cards.

2. Address Verification: Proof of address, such as utility bills or bank statements, may be required to verify the customer’s residential or business address.

3. Purpose of Transactions: Understanding the purpose of the transactions or business relationship helps assess whether it aligns with the customer’s profile and expected activities.

4. Risk Assessment: KYC also includes assessing the potential risk associated with a customer, which can help determine the level of due diligence required.

Now, let’s discuss why KYC is relevant for small businesses when making payments to contractors:

1. Legal Compliance: Many countries and regions have regulations in place that require businesses to conduct KYC on their clients or contractors. Failing to comply with these regulations can lead to legal and financial penalties.

2. Risk Mitigation: KYC helps small businesses assess the risk associated with their contractors. By verifying the identity and legitimacy of contractors, businesses can reduce the risk of hiring fraudulent or untrustworthy individuals or entities.

3. Fraud Prevention: Small businesses can be vulnerable to fraud, including invoice fraud and payment scams. KYC helps identify potentially fraudulent contractors and reduces the likelihood of falling victim to such scams.

4. Reputation Management: Ensuring that contractors are legitimate and have a clean history can help protect a small business’s reputation. Engaging with contractors who engage in illegal activities can harm a business’s image.

5. Access to Financial Services: Small businesses may need to open business bank accounts or obtain financing. Many financial institutions require KYC documentation to provide these services, so having proper KYC records in place is essential.

In summary, KYC is relevant for small businesses when making payments to contractors because it helps them comply with regulations, mitigate risks, prevent fraud, protect their reputation, and access financial services. By verifying the identity and legitimacy of contractors, small businesses can make more informed decisions and conduct transactions with confidence.

What is KYB (“Know Your Business”)?

KYB stands for “Know Your Business” or “Know Your Customer’s Business.” It is a process that businesses and financial institutions use to verify the identity and legitimacy of other businesses or entities with which they conduct transactions. KYB is an extension of KYC (Know Your Customer) and is focused on understanding and assessing the business entities a company interacts with. This means knowing the business involved, some examples include questions around a business’s corporate structure, legal entity, state of incorporation, or ownership structure. Here’s why businesses need to understand KYB when making payments and engaging with other businesses:

1. Regulatory Compliance: Just as KYC is essential for individuals, KYB is crucial for businesses to comply with anti-money laundering (AML), counter-terrorism financing (CTF), and other financial regulations. Many countries require businesses to perform due diligence on their business clients and partners to prevent illegal activities.

2. Risk Mitigation: Understanding the businesses you are dealing with helps assess and mitigate potential risks. KYB allows companies to evaluate the financial stability, reputation, and legitimacy of their business partners, reducing the risk of fraud or doing business with entities involved in illegal activities.

3. Fraud Prevention: Verifying the identity and authenticity of business entities helps protect against various types of fraud, including invoice fraud, supplier fraud, and business identity theft. Businesses can avoid making payments to fraudulent or unverified entities.

4. Credit and Supplier Assessment: Companies often rely on credit and trade references when making payments or entering into contracts with other businesses. KYB helps in assessing a business’s creditworthiness, financial stability, and reliability as a supplier or partner.

5. Reputation Management: Associating with businesses involved in illegal or unethical activities can damage a company’s reputation. KYB allows businesses to screen potential partners and suppliers to ensure they align with the company’s values and standards.

How can Payment Labs help with KYC/KYB?

Our fully compliant fintech solution can significantly streamline and automate the KYC (Know Your Customer) and KYB (Know Your Business) processes for small businesses looking to make payments to contractors both domestically and internationally. Here’s how such a solution can help:

1. Digital Onboarding: Fintech platforms can offer digital onboarding for both individual contractors and business entities. Small businesses can collect required documentation and information electronically, reducing the need for physical paperwork.

2. Data Verification: These platforms can utilize advanced data analytics and verification tools to authenticate the identity and legitimacy of contractors and business partners. This includes checking identity documents, verifying addresses, and cross-referencing data against various databases.

3. Risk Assessment: Payment Labs can automate risk assessment by assigning risk scores to contractors and businesses based on various factors, such as their industry, geographic location, financial stability, and previous transaction history. This helps businesses make informed decisions about engaging with contractors.

4. Compliance Checks: The solution can automatically conduct compliance checks to ensure that contractors and business partners adhere to local and international regulatory requirements. This includes sanctions screening, politically exposed person (PEP) checks, and AML (Anti-Money Laundering) checks.

5. Document Management: Fintech platforms can help businesses store and manage all KYC and KYB documents securely in a digital format, making it easy to access and retrieve information when needed.

6. Automated Updates: The solution can provide automated alerts and updates when documents or information expire or need to be reviewed, ensuring that businesses remain compliant over time.

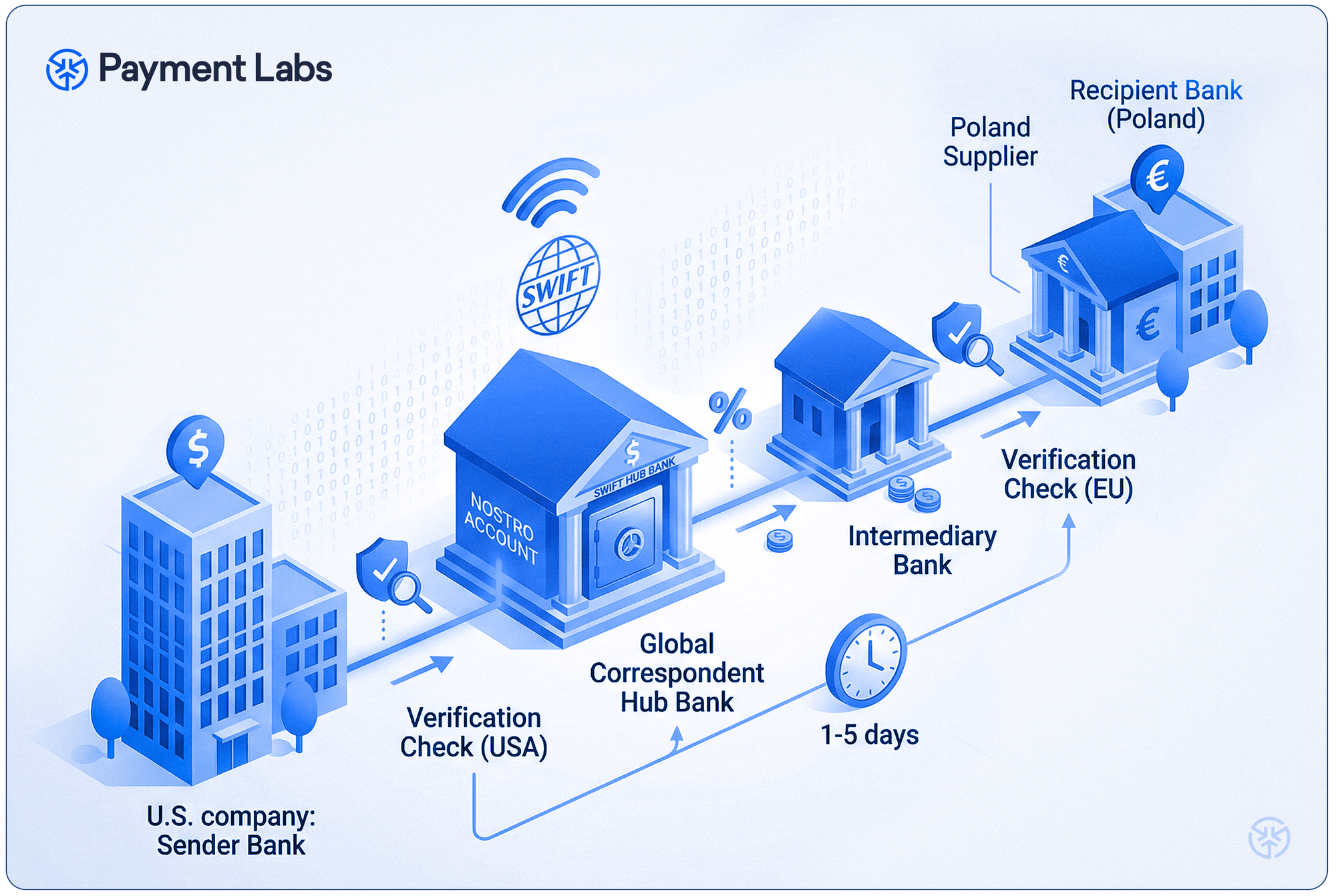

7. Cross-Border Capabilities: For international payments, Payment Labs makes payments to 95 countries in 70 currencies, allowing payees to be paid in their local currency, offering compliance with foreign regulations and seamless cross-border payments, simplifying the payment process for contractors located in different countries. When businesses engage in international trade or cross-border transactions, KYB becomes even more critical. It helps ensure compliance with international regulations and mitigates risks associated with dealing with foreign entities.

8. Integration with Payment Systems: Payment Labs can integrate with various payment systems, allowing small businesses to initiate payments directly from the platform. This integration streamlines the payment process and ensures that payments are made to verified and compliant recipients.

9. Reporting and Audit Trail: Fintech platforms can generate reports and maintain an audit trail of all KYC and KYB activities, making it easier for businesses to demonstrate compliance to regulators and auditors.

10. Access to Financial Services: Businesses may require financial services such as loans, credit lines, or merchant accounts. Financial institutions often require KYB information to provide these services, so having proper KYB records is essential for accessing financial resources.

11. User-Friendly Interfaces: User-friendly interfaces and dashboards make it easy for small businesses to navigate and manage the KYC and KYB process efficiently.

12. Scalability: Payment Labs is scalable, accommodating the needs of SMBs as they grow and interact with more contractors and business partners.

13. Cost Savings: By automating these processes, small businesses can reduce the administrative overhead associated with manual KYC and KYB checks, leading to cost savings.

In summary, KYC and KYB is essential for businesses when making payments and conducting transactions because it helps them comply with regulations, assess and mitigate risks, prevent fraud, evaluate business partners, manage their reputation, and access financial services. By verifying the identity and legitimacy of other businesses, companies can make informed decisions and protect themselves from legal and financial risks.

Want to see how Payment Labs can work for your business? Reach out and talk with one of our Payment Experts today!