How correspondent banking works and how to reduce cross-border payment costs

You send a wire transfer to a supplier. Your bank charges you a fee and estimates it will take three business days. The payment arrives late, and your supplier says they received less than you sent.

This is a common experience with international transfers. But it’s not all up to your bank. Most cross-border payments move through a chain of financial institutions before reaching the final destination. Each intermediary may deduct fees, apply foreign exchange margins, or delay the payment with compliance checks.

This system is known as correspondent banking.

On a high level, correspondent banking is a global network that allows banks to deliver transactions in different countries and currencies. When two banks don’t have a direct relationship, they rely on intermediaries to settle transactions on their behalf. This process includes messaging networks, prefunded accounts, local payment rails, and multiple participants.

Knowing how correspondent banking works helps understand:

- What can cause delays in international transfers

- Where hidden fees and currency exchange markups come from

- Why the final amount received may differ from what was sent

- How to reduce costs and improve predictability

Why correspondent banking exists

Banks are licensed and regulated within specific jurisdictions, and must operate under their home country’s regulatory framework. Very few institutions have the scale, capital, or need to maintain a physical presence in every market and currency they work with.

Instead of building a global infrastructure for themselves, banks establish correspondent relationships with local institutions that already work inside those jurisdictions.

A correspondent bank complies with local regulations and provides its partners with access to domestic clearing systems, offering services like:

- Cross-border wire transfers

- Currency exchange

- Trade finance

- Cash and treasury management

- Access to payment systems

Through correspondents, foreign banks can do all this without opening branches or obtaining a local banking license.

Providing currency access to correspondents

At its core, correspondent banking provides access to foreign currencies and local clearing systems. If you need to move euros from a bank that isn’t in the eurozone, your bank needs a correspondent that is a part of it.

To make this possible, your bank maintains a prefunded account (a nostro account) with a correspondent in that currency.

- If the payee’s bank uses the same correspondent, settlement is simply a ledger adjustment within that institution.

- If the payee uses a different correspondent, funds move between them through domestic payment rails to the beneficiary bank.

Correspondent bank vs intermediary bank

The terms correspondent and intermediary bank are often used interchangeably but they describe slightly different roles within the payment flow.

A correspondent bank maintains an ongoing relationship with another bank. This typically includes:

- Prefunded interbank accounts (nostro/vostro accounts)

- Established payment, FX, and compliance processes

- Access to specific currencies and clearing systems

This is a standing, long-term partnership, rather than a relationship arranged per transaction.

An intermediary bank fills the gap when the sender’s correspondent doesn’t hold an account of the payee’s bank. It is any institution that helps route a specific payment when a direct settlement path does not exist between the correspondent bank and the payee’s bank.

In that case, the payment moves through one or more intermediaries until it reaches a bank that can credit the payee. Intermediaries are selected from the broader network of institutions with which your correspondent has a relationship and can use to efficiently route payments.

Nostro and vostro accounts

The foundation of correspondent banking is two banks holding accounts with each other. When your bank holds an account at a foreign correspondent bank in a specific currency, that is called a nostro account (our money at your bank). From the correspondent bank’s perspective, this is a vostro account (your money held at our bank).

To make sure money can move quickly, these accounts are prefunded. Your bank buys currency on the FX market and deposits it into its nostro account. When you send a wire, your bank instructs the correspondent to take the amount out of their account and credit the next bank in the chain.

To keep the system operational, your bank has to keep money in nostro accounts across multiple currencies and institutions. Managing these balances and the tied-up liquidity accounts for a large portion of correspondent banking costs.

The role of hub banks

Correspondent banking is dominated by a small number of global banks like JPMorgan Chase, Citibank, HSBC, or Deutsche Bank. They operate as hub banks connecting smaller institutions to a large network of intermediaries worldwide.

Banks maintain nostro accounts with these hubs to better manage liquidity and access multiple currencies and local clearing systems with a minimal number of intermediaries.

How correspondent banking works (step-by-step)

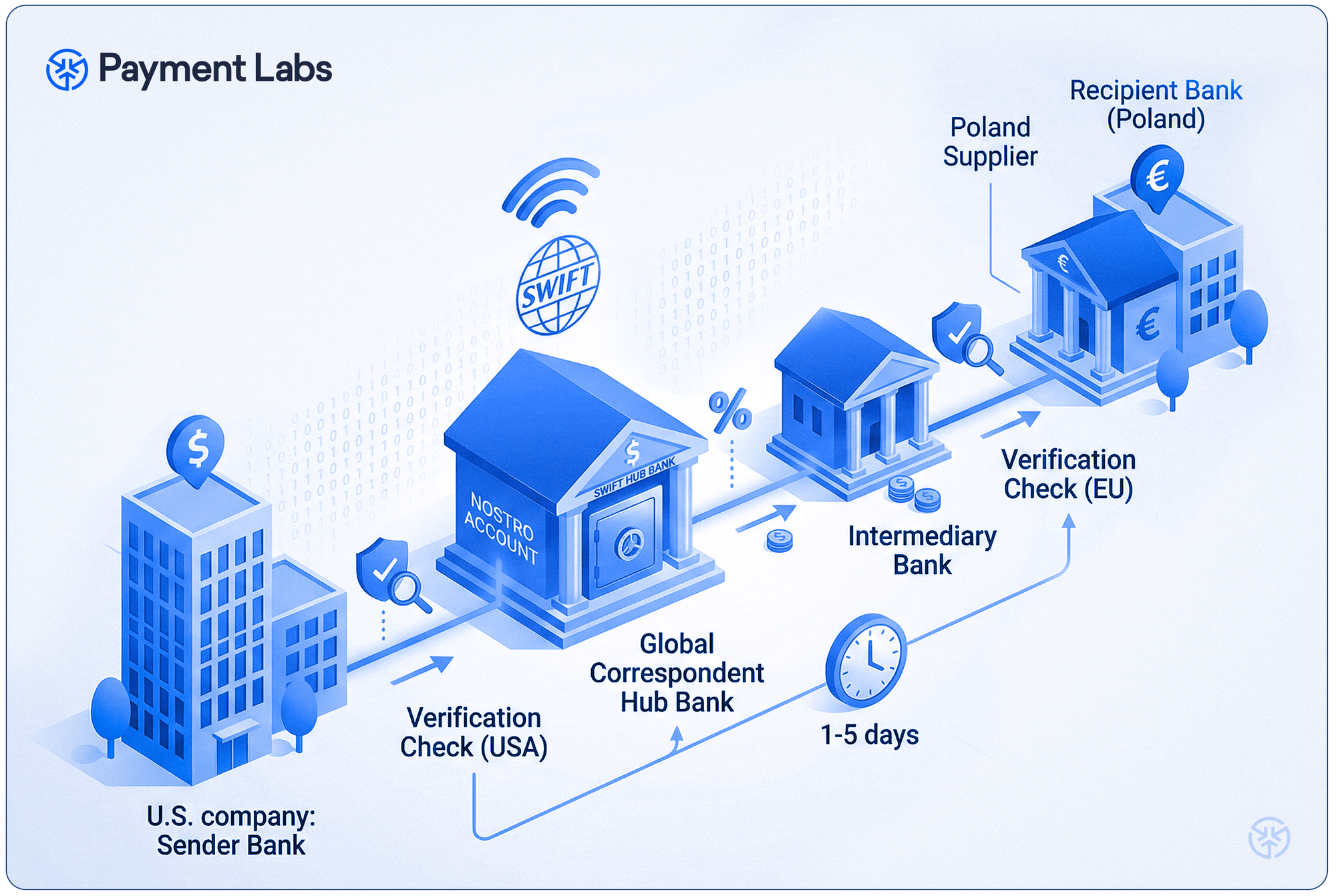

Let’s say a U.S. company sends euros to a supplier in Poland.

- The U.S. bank doesn’t have a direct relationship with the supplier’s Polish bank.

- The U.S. bank routes the payment through its euros-denominated nostro account in a large correspondent, like Citibank.

- SWIFT is used to communicate instructions and track the payment.

- If Citibank has a direct link with the payee’s bank, it credits their account. If not, it passes the money through one or more intermediaries until it reaches the payee.

- Each participant in the chain deducts their fees, reducing the final amount received.

Relations between correspondent banking and SWIFT

Correspondent banking describes a relationship between banks, while SWIFT is a messaging network that allows banks to communicate instructions and track payments.

Most correspondent banks rely on SWIFT as the dominant standard for international bank communications, though some use alternative or proprietary messaging systems based on bilateral agreements.

In 2017, SWIFT introduced GPI (Global Payment Innovation), adding end-to-end payment tracking so banks can see exactly where a payment is in the chain and what fees were deducted. Banks not connected to SWIFT can still exchange transaction information through other channels.

Calculating the real costs of correspondent banking

The fee your bank quotes for a wire transfer rarely reflects the total cost of the transaction. Additional charges can include:

- Lift fee: your bank’s charge for initiating and managing the transfer.

- Correspondent fee: charged by the correspondent bank handling the transaction.

- Intermediary deductions: applied by each bank in the payment chain.

- FX markups: exchange rate markups include 3-5% margins.

- Reciprocal fees: charged to the payee’s bank for processing the payment.

- Double conversion: if no direct market exists, the payment may convert to USD and then to the destination currency, doubling the FX markup.

- SWIFT messaging fees: paid by banks for sending payment instructions.

Who pays these fees depends on the fee structure selected when the wire is initiated:

- OUR: the sender pays all the fees

- SHA (shared): sender covers their own bank’s fees, and the payee covers the correspondent and intermediary fees.

- BEN (beneficiary): payee pays all fees from the transferred amount.

How to minimize correspondent banking fees

- Negotiate with your bank: if you’re sending cross-border payments regularly, you can discuss lower wire fees and better FX margins.

- Use OUR when it matters: when it’s critical that the full amount reaches the payee, cover all the fees.

- Ask for correspondent details upfront: knowing which correspondent your bank uses can help you choose a bank with fewer intermediaries.

- Consolidate payments: sending one larger payment is often cheaper than multiple smaller ones.

- Explore alternatives: for high-cost corridors, fintech solutions may offer faster transactions and lower fees.

How long do transactions via correspondent banking take

Most correspondent transfers settle within 1-5 business days, though same-day processing is possible for certain currencies and cutoff windows.

The timing depends on factors like:

- the number of intermediaries

- currency-specific cutoff times

- time zone differences

- compliance checks and screenings

- local holidays

- correspondent processing windows.

To speed up your transfer, initiate it early in the day and avoid Fridays or holidays for time-sensitive payments.

Correspondent banking alternatives

Depending on the destination and amount, faster and cheaper alternatives to traditional correspondent banking are available.

- Fintech platforms: For individuals and small businesses, these platforms avoid correspondent banking by maintaining local accounts in multiple countries. They offer transparent fees and exchange rates closer to the mid-market. However, they may impose limits on supported payment corridors and transaction volumes.

- Enterprise payment infrastructure: For high-volume businesses, enterprise payment systems use local FBO accounts across many countries, providing better FX rates and faster settlement than banks. At scale, these systems can offer substantial savings compared with correspondent banking.

Key takeaways

- Correspondent banking allows institutions without direct relationships to send cross-border payments.

- Fees are often hidden and can be covered by the sender, the payee, or shared.

- Payment timing depends on the number of intermediaries, time zones, compliance checks, and local holidays.

- You can reduce costs by negotiating fees, consolidating payments, using alternatives, and choosing better payment routes.

- Individuals and high-volume businesses have options that can be faster, cheaper, and more transparent than correspondent banking.